In this article:

- What Is a Subprime Mortgage?

- How Do Subprime Mortgages Work?

- What Credit Score Do You Need for a Subprime Mortgage?

- What Are the Types of Subprime Mortgages?

- Subprime Mortgage vs. Prime Mortgage

- Pros and Cons of Subprime Mortgages

- Should You Get a Subprime Mortgage?

- How Do I Get a Subprime Mortgage?

- Alternatives to a Subprime Mortgage

A subprime mortgage is a home loan designed for borrowers with poor or limited credit history. Because lenders take on more risk with these borrowers, subprime mortgages typically come with higher interest rates, higher fees and stricter down payment requirements than conventional "prime" mortgages. Here's what you should know before you apply.

What Is a Subprime Mortgage?

A subprime mortgage is a home loan offered to borrowers with poor credit. Though the definition of a subprime borrower varies from one lender to the next, subprime mortgages may be available to borrowers with a FICO® Score☉ Θ below 670.

The term "subprime mortgage" fell out of favor following the 2008 financial crisis, so subprime mortgages are sometimes advertised as "nonprime." Some subprime mortgages are classified as nonqualified mortgages, indicating lenders must provide strict documentation of borrowers' ability to repay the loans.

Learn more: What Does Subprime Mean?

How Do Subprime Mortgages Work?

Pricing on subprime mortgages can vary by mortgage type, but all subprime mortgages share these attributes:

- Higher interest charges: Rates on subprime mortgages are typically several percentage points higher than those on conforming mortgages.

- Higher closing costs: Lenders offset some of the risk by collecting high fees upfront, such as origination fees.

- Higher down payment requirements: Borrowers with outstanding credit may be able to finance a home by putting down as little as 3% of the purchase price, but subprime borrowers may be required to put down 25% or more.

You can apply for subprime mortgages at banks, credit unions and online lenders. Subprime borrowers typically undergo a stricter underwriting process as lenders want to make sure you can repay the loan.

Tip: Lending standards vary, so it's worth shopping around. You might qualify for a conventional mortgage with one lender even if another only offers you a subprime loan, and subprime terms can differ significantly from lender to lender.

What Credit Score Do You Need for a Subprime Mortgage?

There is no universal minimum credit score for a subprime mortgage, as each lender sets its own standards. That said, subprime mortgages are generally available to borrowers with FICO® Scores below 670, and some lenders will consider applicants with scores as low as 500.

If your score is below 620, expect lenders to scrutinize other parts of your financial profile more closely, including your debt-to-income (DTI) ratio, employment history and cash reserves. A lower score often means a higher down payment will be required as well.

Learn more: What Credit Score Do I Need to Buy a House?

What Are the Types of Subprime Mortgages?

Here are three kinds of subprime mortgages you may come across while researching your options.

Adjustable-Rate Mortgage (ARM)

ARMs start out with relatively low payments for a number of years (five, seven and 10 years are common) based on an introductory interest rate; then the interest rate adjusts periodically for the remainder of the loan term.

ARM interest rates—and their monthly payments—typically reset every six or 12 months following the initial fixed-rate period, rising or falling in sync with the relevant index the lender uses to determine rates. The maximum annual increase is capped by federal regulation, but shifting payments can put strain on household budgets.

Keep in mind that ARMs aren't exclusive to subprime mortgages. You can also get an ARM if you have good credit.

Learn more: Common Types of Adjustable-Rate Mortgages

Extended-Term Mortgage

These loans may come with fixed interest rates but feature repayment terms of 40 years, instead of the 30-year norm for conventional mortgages.

Over the life of the loan, that can mean hundreds of additional payments, and interest compounding for an extra decade or more, with the potential to cost hundreds of thousands of dollars more than a conventional loan.

Interest-Only Mortgage

Similar in structure to an adjustable-rate mortgage, an interest-only mortgage provides low initial payments by giving you the option to pay only interest due on the loan (without any principal payments) for the first five to 10 years of the loan term. At the end of this introductory period, you can renew the loan or refinance, but you must begin paying down principal.

Interest-only mortgages work best if you make standard interest-plus-principal monthly payments and only resort to lower interest-only payments in cases of emergency. If home prices are declining in your neighborhood, you might even find yourself upside down on the loan and possibly even facing a short sale or foreclosure.

†The information provided is for educational purposes only and should not be construed as financial advice. Experian cannot guarantee the accuracy of the results provided. Your lender may charge other fees which have not been factored in this calculation. These results, based on the information provided by you, represent an estimate and you should consult your own financial advisor regarding your particular needs.

| Adjustable-Rate Mortgage | Extended-Term Mortgage | Interest-Only Mortgage | |

|---|---|---|---|

| Term | 30 years | 40 years | 15 or 30 years |

| Interest rate | Fixed intro rate, then resets periodically | Fixed over a longer term | Fixed during interest-only period, then adjusts |

| Payment structure | Payments reset regularly after the intro period | Same as conventional, but spread over 40 years | Interest-only payments required for first five to 10 years; principal-and-interest after |

| Equity | Builds gradually as loan amortizes | Builds gradually, but more slowly than a 30-year loan | No equity on interest-only payments; builds gradually once principal payments begin |

| Best for | Borrowers expecting income growth to cover future payment increases; borrowers who plan to move or refinance in a few years | Buyers who can't qualify for shorter terms and plan to refinance later | Borrowers who want payment flexibility but intend to pay principal when possible |

Subprime Mortgage vs. Prime Mortgage

The biggest difference between a subprime mortgage and a prime mortgage comes down to risk. Prime mortgages are offered to borrowers that lenders consider low risk—those with strong credit, stable income and a manageable debt load. Subprime mortgages serve borrowers who don't meet those standards, and the loan terms reflect that additional risk.

Credit Score Requirements

Lenders set their own minimum score requirements, but prime loans are generally available to borrowers with FICO® Scores of 670 or greater. Subprime mortgages may be available to borrowers with credit scores as low as 500.

Learn more: What Are the Different Credit Score Ranges?

Down Payment Requirements

For prime mortgages, lenders routinely accept down payments as low as 3% with a requirement that the buyer pay for mortgage insurance if they put less than 20% down. By contrast, on subprime mortgages, down payment requirements of 25% or more of the purchase price are not uncommon.

Learn more: How Your Down Payment Affects Your Mortgage

| Feature | Subprime Mortgage | Prime Mortgage |

|---|---|---|

| Credit score required | Generally below 670; some lenders accept scores as low as 500 | Typically 670 or higher |

| Down payment required | Often 25% or more | As low as 3%, though 20% avoids private mortgage insurance (PMI) |

| Interest rate | Significantly higher than benchmark rates | Near or in line with current benchmark rates |

| Loan types available | Often ARMs, extended-term or interest-only loans | Fixed-rate and adjustable-rate options widely available |

| Underwriting | More documentation and scrutiny required | Standard underwriting process |

Prime mortgages generally offer more favorable terms across the board. If you're close to the subprime/prime threshold, it's worth taking time to improve your credit before applying. Even a modest score increase can unlock better rates and lower lifetime costs.

Pros and Cons of Subprime Mortgages

If you're considering a subprime mortgage, it's important to weigh the potential benefits and drawbacks of accepting such a loan.

Pros

Enables homeownership: Subprime mortgages offer a pathway to homeownership when you can't qualify for a conventional home loan. If you haven't established a substantial credit history or if your credit scores are damaged from past mishaps or missteps, a subprime loan may be your only mortgage option.

Credit score benefits: If you keep up with your mortgage payments and manage other debt wisely, you'll likely see improvement in your credit scores. Regular on-time mortgage payments will help you build a positive payment history, and payment history is the single largest factor influencing credit scores, responsible for up to 35% of your FICO® Score.

Path to better financing: A subprime mortgage can serve as a stepping stone. If you make consistent on-time payments and improve your credit over time, you may eventually qualify to refinance into a conventional loan with a lower (or at least fixed) interest rate.

Cons

Cost: Charges on subprime mortgages can be significantly higher than those on prime loans, potentially costing you tens or even hundreds of thousands of dollars more than a conventional mortgage on the same property.

Budgeting challenges: The annual rate reset on an ARM and the shift to higher required payments following the intro period on an interest-only mortgage may put stress on many household budgets. If you go either route, plan carefully and do your best to set aside funds to help cushion major payment hikes.

Slow equity accumulation: Early payments on amortized loans like mortgages are mostly interest, with just a small portion going toward principal. Payments toward the end of the loan term are mostly principal, with just a small share of interest. Home equity—the portion of the home you own—accumulates as you pay down principal. An extended-term loan stretches this process out significantly.

Should You Get a Subprime Mortgage?

A subprime mortgage isn't right for everyone, but it may make sense in certain situations. Consider a subprime mortgage if:

- You've been unable to qualify for a conventional mortgage after applying with multiple lenders.

- You need to buy a home now and have a clear plan to refinance once your credit improves.

- You can comfortably afford the higher monthly payments and down payment requirements.

- You understand and accept the loan's terms, including any rate adjustment caps or prepayment penalties.

When to Avoid a Subprime Mortgage

A subprime mortgage comes with real costs and risks, and it isn't always your only option. Skip the subprime route if:

- You haven't yet applied with multiple conventional lenders—lending standards vary, and you may qualify for a standard loan elsewhere.

- You haven't explored government-backed options like FHA or VA loans.

- You can realistically improve your credit score within six to 12 months.

- You're being offered an extended-term mortgage and aren't prepared for how slowly equity builds over a 40-year repayment period.

- The monthly payment would strain your budget even before any rate adjustments.

| Loan Term | Equity After 30 Years |

|---|---|

| 30 years | 100% |

| 40 years | 46% |

If you decide to seek a subprime mortgage, make sure you understand its terms clearly, including the potential for payment increases. Pay close attention to any prepayment penalties and how much they could cost you if you refinance in the future.

Learn more: How to Buy a House: Step-by-Step Guide

How Do I Get a Subprime Mortgage?

Applying for a subprime mortgage follows much the same process as applying for a conventional loan. Here's what you'll typically need:

- Proof of income: This may include recent pay stubs, W-2s or tax returns to verify your earnings.

- Employment verification: Includes any documentation confirming your current employment status and work history.

- Bank statements: You'll usually need two to three months of statements showing cash reserves and regular income.

- Credit history: Lenders will pull your credit reports; be prepared to explain any negative items such as late payments, collections or a prior foreclosure.

- Down payment funds: Subprime lenders often require 25% or more down, and you'll need to document where the money is coming from.

- Debt documentation: Collect records of any existing debts, including student loans, auto loans and credit card balances.

Once you've gathered your documents, you can apply through banks, credit unions or online lenders that specialize in nonprime loans. Compare offers from multiple lenders, as rates and terms can vary significantly.

Alternatives to a Subprime Mortgage

Before settling on a subprime mortgage, it may be worth considering some of these other options, which could be more affordable and less risky.

Get a Cosigner

If you cannot qualify for a conventional mortgage on your own, getting a relative or friend with good credit to act as a cosigner might help you avoid a subprime loan.

A cosigner's credit scores and income are considered along with yours when determining loan eligibility. You're still considered the primary borrower and owner of the house, but a cosigner shares equal responsibility with you for ensuring your loan is repaid. If you fail to make payments, your cosigner's credit scores will also suffer, and the cosigner can be pursued for payment.

FHA Loans

Insured by the Federal Housing Administration (FHA), FHA loans have a minimum credit score of 500 if you make a 10% down payment on your purchase. If you put down less than that, the minimum credit score required is 580.

They do, however, come with higher mortgage insurance requirements than some conventional loans, and you'll pay for this insurance longer the less you put down.

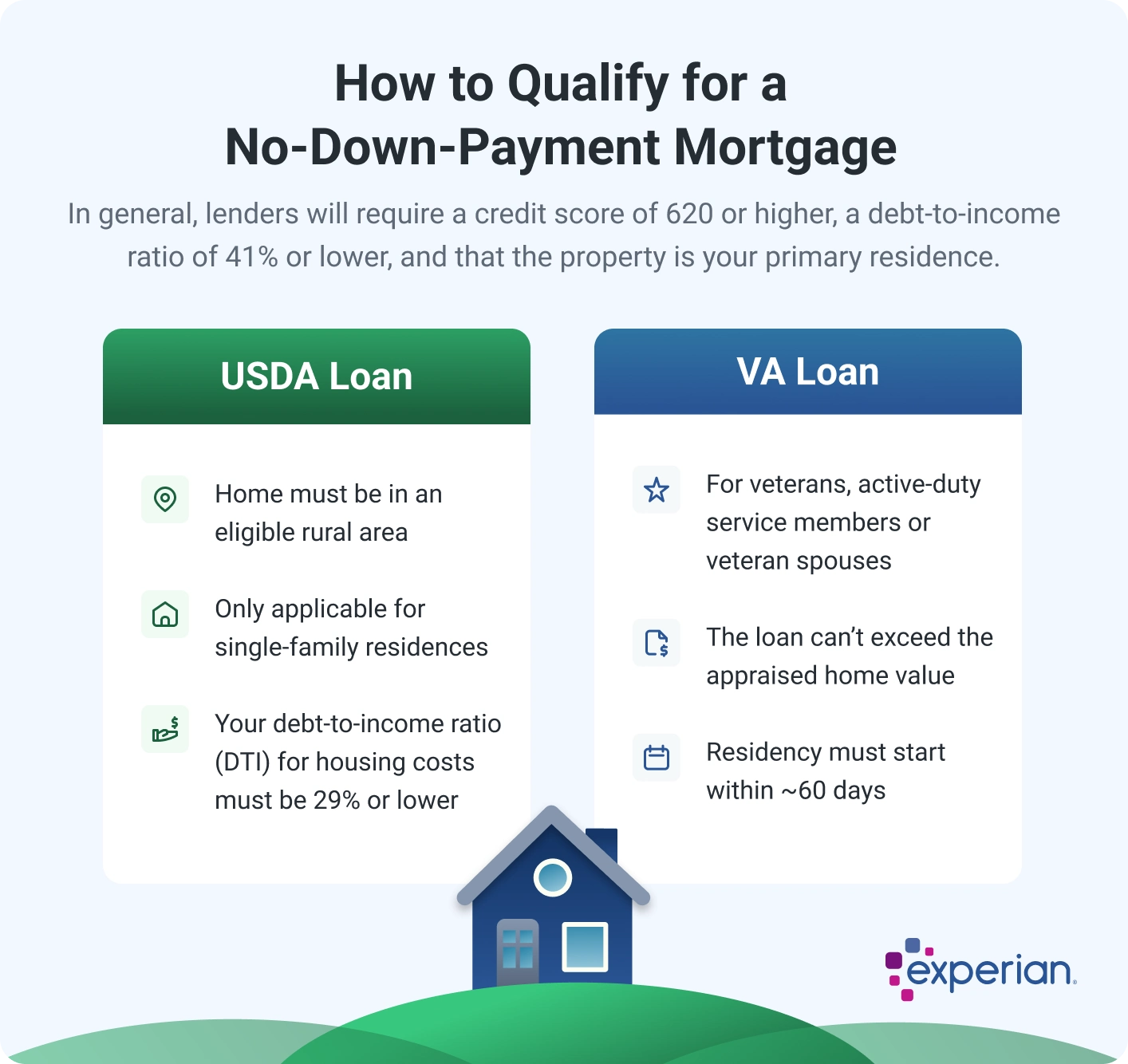

VA Loans

VA loans are backed by the U.S. Department of Veterans Affairs (VA) for select members of the military community, their spouses and other eligible beneficiaries.

There's no minimum credit score set by the VA, but lenders who provide VA loans typically seek scores of 620 or higher. Borrowers must also meet other eligibility requirements related to their military service or that of a family member.

USDA Loans

The U.S. Department of Agriculture (USDA) backs mortgages, known as USDA loans, for buyers with low to moderate incomes seeking to buy designated rural properties. The USDA does not require a minimum credit score, and lenders may accept applicants with scores as low as 580, although some require scores of at least 640.

Frequently Asked Questions

What Is Considered Subprime Credit for a Mortgage?

There's no single industry standard, but subprime borrowers are generally those with FICO® Scores below 620. Factors beyond your credit score—like your DTI ratio and down payment—also influence how a lender classifies you.

Where Can I Get a Subprime Mortgage?

Subprime mortgages are available from many of the same sources as conventional home loans, including banks, credit unions, dedicated home finance companies and online lenders that specialize in nonprime or nonqualified loans.

Why Do Subprime Mortgages Have Higher Interest Rates?

Lenders view the lower credit scores common to subprime applicants as a sign of higher repayment risk. To offset the greater chance of default, lenders charge higher interest rates on subprime mortgages than they do on prime loans.

Are Subprime Mortgages Risky?

Subprime mortgages carry more risk than conventional loans for both borrower and lender. Higher rates, adjustable payments and longer loan terms can strain your budget and slow equity growth. Carefully review all loan terms and compare multiple offers before committing.

Can You Refinance a Subprime Mortgage?

Yes. If your credit improves after taking out a subprime mortgage, you may be able to refinance into a conventional loan with a lower interest rate. Consistent on-time payments over time are one of the most effective ways to build the credit needed to qualify for better terms.

Take Control of Your Credit Before You Apply

If your credit scores are low and a subprime mortgage is the only type of home loan you qualify for, the loan may be your best opportunity to become a homeowner in the immediate future. Because these loans carry high interest rates and potential for shifting payment amounts, managing them can be challenging and expensive.

Before applying, you can check your Experian credit report and FICO® Score for free with Experian. Use what you find there as a guide to improving your credit. Even modest gains could open the door to better loan terms and lower costs over the life of your mortgage.